2025 was a significantly better year for mortgage borrowers in Poland than 2024. The National Bank of Poland reduced the base rate several times during 2025, bringing it down from 5.75% to 4.00%.

As a result, mortgage interest rates also declined. This reduced monthly payments for existing borrowers and improved affordability for those applying for a mortgage for the first time.

MORTGAGE RATES

At the time of writing 5-year fixed-rate mortgages in Poland range from 5.64% to 6.16% depending on a size of your deposit and the bank. There are also special offers at some banks for re-mortgaging starting at 5.49%, and for energy-efficient properties starting at 5.42%.

For variable-rate mortgages banks typically offer margin between 1.50% and 2.30%. Current variable rates in Poland are between 5.57% and 6.03%. Margins for re-mortgaging start at 1.50%, and for energy-efficient properties start at 1.30%.

In Poland variable-rate mortgage interest rate is calculated this way:

Mortgage rate = WIBOR + bank’s margin

Bank’s margin is fixed, WIBOR is variable. So your mortgage interest rate moves automatically in line with WIBOR. At the time of writing (6th of February 2026) WIBOR is 3.78% – 4.00% depending on the type of WIBOR.

The table below shows current mortgage rates from leading banks in Poland.

The above rates may not be suitable for your circumstances and might not be available when you’re ready to submit an application.

Please remember that the best mortgage deal is not only about the lowest interest rate. You should look at all costs and the bank’s requirements in the mortgage offer.

AFFORDABILITY

Lower interest rates mean lower monthly mortgage payments. That’s why you can get a higher mortgage amount with the same income.

Currently most borrowers in Poland can expect to be able to borrow up to around 6 times their net annual income. However, there are other important factors which affect affordability including age, debt, dependants, credit score and employment status.

Below there are examples of the maximum mortgage amount possible to borrow in different scenarios (assuming no other loans, applicants aged 20 – 40, employed on contract):

Single person

Monthly net income → Max loan

5,000 PLN → 379,000 PLN

7,000 PLN → 570,000 PLN

10,000 PLN → 820,000 PLN

13,000 PLN → 1,050,000 PLN

Couple without children

Monthly net income (combined) → Max loan

8,000 PLN → 590,000 PLN

11,000 PLN → 900,000 PLN

15,000 PLN → 1,230,000 PLN

20,000 PLN → 1,640,000 PLN

Couple with children

Monthly net income (combined) → Max loan

8,000 PLN → 470,000 PLN

11,000 PLN → 830,000 PLN

15,000 PLN → 1,230,000 PLN

20,000 PLN → 1,640,000 PLN

Pleas bear in mind that the presented amount may not be suitable for your circumstances and might not be available when you’re ready to submit an application.

If you want to know the maximum mortgage amount you can get based on your individual situation you can contact me. I will calculate it for you.

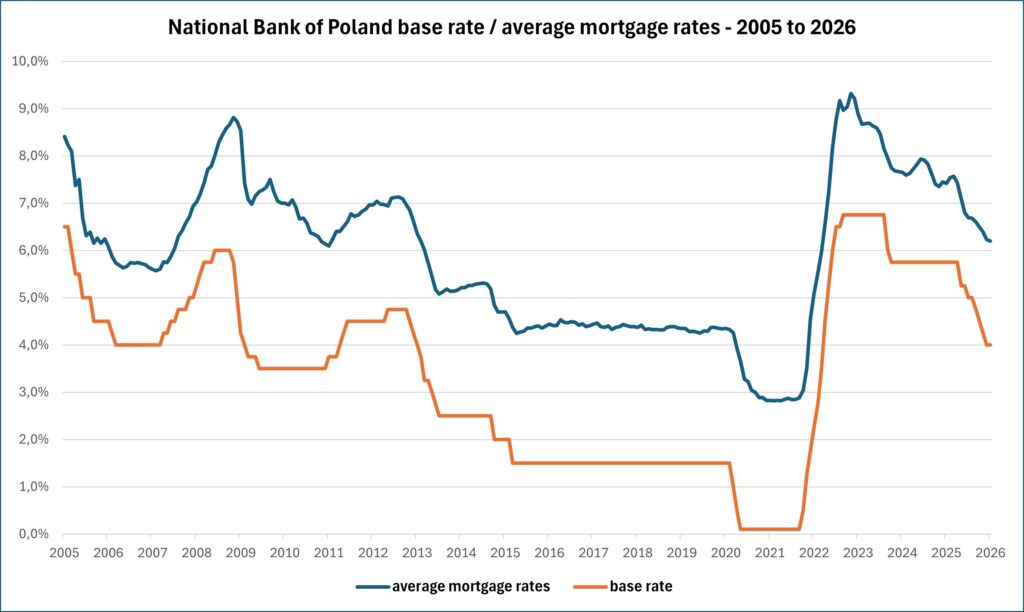

INTEREST RATES IN POLAND. WHERE ARE WE NOW?

The current National Bank of Poland base rate is 4.00%.

The chart below shows how the National Bank of Poland base rate and average mortgage rates in Poland changed over time.

What next for interest rates in Poland?

Everything depends on inflation, but fortunately inflation is still falling in Poland. In December 2025, inflation went down to 2.4% on a yearly basis (compared to 2.5% in November). With the base rate at 4.0%, which is quite high compared to other European countries, we still have room for a further interest rate decrease. Most analysts say that this is only a matter of time.

These are some of the predictions for Polish base rate this year:

- Fitch Ratings expects base rate will drop to 3.75% in 2026.

- Bank Gospodarstwa Krajowego predicts base rate will fall to 3.50% in the second quarter of 2026.

- ING Bank expects a decrease to 3.25% or lower in 2026.

- PKO Bank Polski and BNP Paribas predicts base rate will fall to 3.50% in the middle of 2026.

- Analysts from mBank expect an even deeper decrease to 3.00% at the end of 2026.

0% DEPOSIT MORTGAGES

In Poland, it is possible to obtain a mortgage with no deposit, provided both the borrower and the property meet specific criteria. You can borrow up to 100% of the purchase price, or even more if you want to add some amount for renovation. This is possible thanks to the Polish Government scheme called “Rodzinny Kredyt Mieszkaniowy”. Find out more about the 0% deposit mortgage in Poland.

The program isn’t very popular in Poland. A lot of clients don’t even know that this program exists. In my opinion, the main reason for this is that the Polish government doesn’t advertise this program. Banks also don’t advertise it. The second reason is that there are limits on the property’s price per square meter. It depends on the location, but it’s not easy to find a property within the set limits. The price limits are different for different cities and different areas in Poland. Bank Gospodarstwa Krajowego announces the limits for every quarter. Price limits for the first quarter of 2026 you will find here.

If you don’t have any deposit, the maximum amount you can borrow in this program is 500,000 PLN, which is usually too low in the biggest cities in Poland. If you buy a property for a higher price, you need to have some deposit. For example, if the purchase price is 600,000 PLN, you need to have a 20,000 PLN deposit; if the price is 700,000 PLN, you need to have a 40,000 PLN deposit (which is still lower than the minimum 10% for a standard mortgage).

On the other hand, the mortgage in this program is a very good option for those who meet the criteria. The mortgage offer is similar (or sometimes even better) to a standard mortgage with a 20% deposit. So with no deposit, or with a deposit lower than 10%, you can get a mortgage offer comparable to an offer with a 20% deposit.

MY THOUGHTS

We don’t have official data for the entire 2025 yet, but for sure it will be a record year in terms of both the number and total value of mortgages granted by banks in Poland.

In 2024, we had very high interest rates in Poland, which in my opinion was the main reason that the mortgage and property market slowed down. But in 2025, the Polish central bank began reducing rates, which led to lower mortgage rates. I think people started to be more optimistic and went back to the market.

Now we have much lower mortgage rates than in 2024, which makes mortgages more affordable. Apart from that, the overall trend remains downward, and there is a high chance that rates will go down further. If rates continue to fall, this could bring even more buyers into the market. That’s why I’m very optimistic, and I think 2026 will be a very good year for the property and mortgage market in Poland.

Of course, the world is unpredictable – but it was and will always be unpredictable. Timing the market is very difficult, but I think it’s a good time to start looking for a property if somebody has held off. There is a high chance that property prices will go up if rates go down.

If you wish to discuss the Polish mortgage market and your plan for this year, feel free to call me on +48 661 440 714 or send me an email at mariusz@mzfinanse.pl