Buying a home in Poland usually requires saving 10%–20% of the purchase price, which can be a real challenge — especially for expats who may have recently moved to the country. A standard apartment in Warsaw can cost 700,000–900,000 PLN, which means a deposit of 70,000–180,000 PLN is usually required. For many people, this is the biggest barrier to entering the property market.

But since May 2022, Poland has introduced a government-backed mortgage program that changes the game. Known as Rodzinny Kredyt Mieszkaniowy (Family Housing Loan), it allows some buyers to take out a 0% deposit mortgage, also called a 100% mortgage. This means you can borrow the entire property price without needing savings for a deposit.

Why was the 0% deposit mortgage introduced?

Polish authorities recognized that younger buyers and families with children often struggle to save for a deposit. At the same time, property prices have been rising quickly, particularly in big cities like Warsaw, Kraków, and Gdańsk. The program was designed to:

- Help first-time buyers enter the market faster.

- Support families with children by making housing more affordable.

- Stimulate the housing market and construction industry.

For expats, this is a unique opportunity, since few countries in Europe currently offer government-backed 100% mortgages.

Key points of the 0% deposit mortgage program

- Minimum deposit: 0%

- Who can apply: First-time buyers and families with children (including some second property buyers)

- Maximum property price: 500,000 PLN (with 0% deposit) or 1,000,000 PLN (if you provide some deposit)

- Government bonus: 20,000 PLN (for 2nd child) or 60,000 PLN (for 3rd+ child born during repayment)

- Property price-per-square-meter limits apply to apartments (different in each region, updated quarterly by BGK)

- Lower mortgage interest rates than standard loans with small deposits.

Benefits of the 0% deposit mortgage

- No deposit required: Normally, buyers must contribute 10–20% of the purchase price as a deposit. This program removes that barrier, making it possible to buy without savings. Even if you have a small deposit (less than 10%), the program can still work for you.

- Government bonus payments: You can receive an additional 20,000 PLN if your second child is born during the mortgage repayment period, or 60,000 PLN if your third (or subsequent) child is born.

- Better mortgage rates: The interest rates offered under this program are generally lower than for standard mortgages with less than 20% deposit.

- Faster entry to the housing market: prices keep rising, so waiting to save a deposit can mean paying more later. In the meantime you usually need to pay for renting.

Are there disadvantages?

While the program is attractive, there are some limitations:

- Not all banks participate. Currently, four banks offer this program to foreigners: Pekao, PKO BP, Santander, and Alior Bank.

- Not all properties are eligible — apartments must fall within official price-per-square-meter limits.

- Income must be earned in Polish zloty (PLN) — foreign currency income does not qualify.

- The mortgage is limited to residential use, not investment-only purchases.

0% deposit mortgage in Poland – who qualifies?

First-time homebuyers

You are considered a first-time buyer if you do not already own a residential property. Even if you owned a home in the past but have already sold it, you are still regarded as a first-time buyer.

You do not qualify if:

- You have had a mortgage within the last 36 months.

- You owned a property and donated it to someone within the last 5 years.

The same rules apply to your properties outside Poland.

Borrowers with children buying a second property

If you already own a property in Poland but have children, you may still qualify — with some restrictions. Restrictions on the size of your current property:

- 2 children → max 50 sqm

- 3 children → max 75 sqm

- 4 children → max 90 sqm

- 5+ children → no restrictions

Eligible applicants

- Single persons

- Married couples

- Unmarried couples with children

Note: Unmarried couples without children cannot apply together.

Eligible Purposes

You may use the mortgage to:

- Buy a residential property

- Buy and renovate/finish a property

- Build a house

Note: For apartments, the purchase price per square meter must not exceed the limit set by BGK (updated quarterly). See BGK price limits here.

For houses (buying or building), there are no per-square-meter limits.

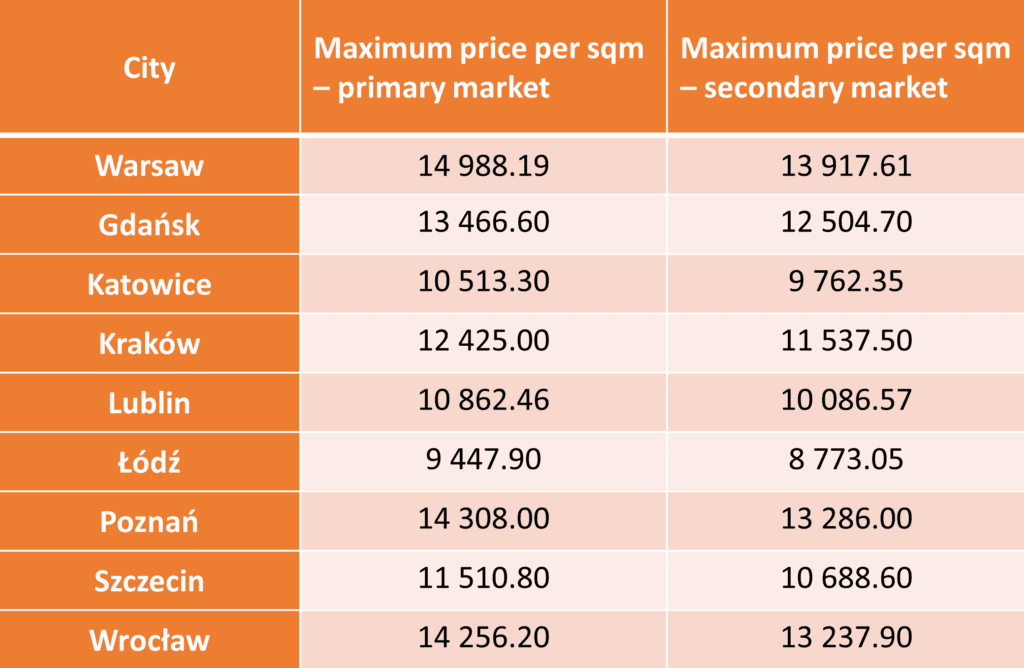

These are the price limits in the third quarter of 2025 for the biggest cities in Poland:

How to increase your chances of approval

Although the program is government-backed, you must still meet standard bank mortgage criteria. Here’s how to improve your chances:

Legal residency

You generally need a residence card (non-EU citizens) or a certificate of residence registration (EU citizens). In some cases, you can apply without these documents, but you must have a PESEL number and a registered address in Poland.

Income in Poland

Your income must be in PLN, earned in Poland. Income from abroad is not accepted.

Save for additional costs

Even with no deposit, you’ll need savings for fees:

- Notary: ~1% of purchase price

- Valuation fee: 0–1,000 PLN (depends on bank and property type)

- Arrangement fee: usually none, but PKO BP charges 0.5%

- Life insurance: usually monthly, but Alior Bank requires 5 years upfront (2.85% of mortgage amount)

- Real estate agent: usually 2–3% of purchase price (not covered by mortgage)

- Other legal fees: ~400 PLN

Work with a mortgage broker

A good broker can check your eligibility, guide you through the process, and handle paperwork. Of course, you can contact me — I’ll gladly help you with this.

FAQ

Can foreigners apply for a 0% deposit mortgage in Poland?

Yes, as long as they live in Poland, earn in PLN, and meet other criteria.

Do I need a permanent residence permit?

No. A temporary residence card (for non-EU) or registration (for EU) is enough. There is also a chance to obtain a mortgage without these documents, but you must have PESEL number and official residential address in Poland.

Can I buy a house instead of an apartment?

Yes — and in this case, there are no price-per-square-meter limits.

How long does the process take?

On average 4–6 weeks, depending on the bank and property documents.

Can I buy property for rental investment?

The program is mainly for residential purposes, but you can rent out a part of your property later (banks usually don’t restrict this).

Final thoughts

The 0% deposit mortgage in Poland is one of the most attractive programs for expats and families who want to buy property but don’t have large savings. It removes the biggest barrier to homeownership — the deposit — while also offering government support and lower interest rates.

For many, this is the difference between waiting years to buy a property and moving into their own home now.

If you’re an expat thinking of buying property in Poland, consider consulting with a mortgage broker. It can make the process smoother, help you avoid mistakes, and give you the best chance of approval. Contact me for a free consultation – I specialize in helping expats successfully get mortgages in Poland.