For the first time in over three years, mortgage rates in Poland have fallen below the symbolic 6% threshold. This marks an important moment for both homebuyers and property investors, as lower rates can significantly improve affordability and borrowing capacity. But what does this mean in practice, and how competitive are the latest offers from banks? Let’s take a closer look.

Interest rates in Poland are falling

In September 2025, the National Bank of Poland cut the base rate by 0.25 percentage points to 4.75% – the lowest since May 2022. At the peak (September 2022 – August 2023), the base rate was as high as 6.75%.

Mortgage rates in Poland have also dropped considerably from their peak. According to data from the National Bank of Poland, in November 2022 the average mortgage rate was 9.32%. The latest report from July 2025 shows the average mortgage rate at 6.69%.

At the time of writing (19 September 2025), most banks still offer mortgages above 6%. On average, 5-year fixed rate is around 6.5%, depending on deposit size and the bank. With at least a 20% deposit, you can expect a rate below 6.5%, but with less than 20% deposit, rates are usually higher. Variable mortgage rates are currently about 0.5% higher than 5-year fixed rates.

The new mortgage offer from BNP Paribas

On 10 September 2025, BNP Paribas launched a new mortgage offer with a 5-year fixed rate starting from 5.9% – but, as always, there are conditions.

Here’s how the discount works. The standard 5-year rate is 6.70%, and you can bring it down if you agree to:

- open a current account and transfer at least 2,500 PLN/month (–0.30%),

- buy life insurance from the bank – required for 3 years, costs 0.04% of the loan balance per month (–0.30%),

- buy property insurance from the bank (0.0075% of the property value per month) (–0.10%),

- buy an energy-efficient “Eco” property (–0.10%).

Put all that together and your interest rate falls to 5.90%.

Now, the first three requirements are pretty standard in Poland. Almost every bank wants you to open an account, transfer income, and take out life insurance. Property insurance is always required, but most banks let you choose your provider – BNP Paribas pushes you to buy it directly from them.

The last one – the “Eco property” discount – is the tricky part. It only applies if the property has an energy performance certificate showing an annual non-renewable primary energy demand of less than 58 kWh/m². In practice, I’ve never seen an apartment that qualifies. Some new houses might, but don’t count on it if you’re buying a flat in Poland.

Example: what does this look like in practice?

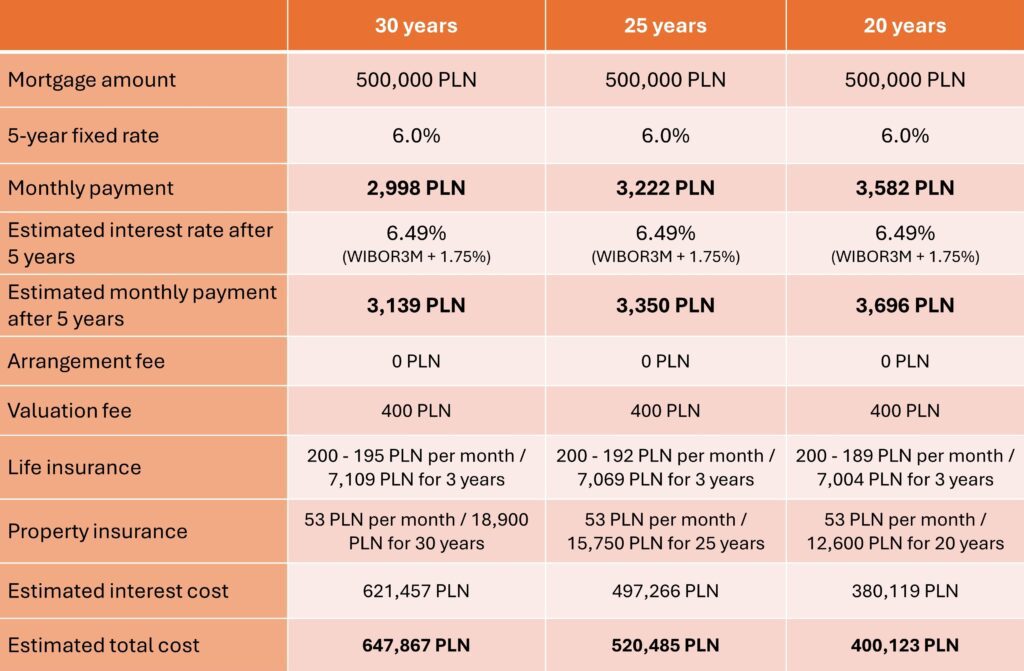

Let’s say you buy a regular apartment (not energy-efficient) for 700,000 PLN and put down 200,000 PLN. That leaves you with a 500,000 PLN loan at a 6.0% fixed rate for the first 5 years.

Here’s what your payments would look like:

Who can actually get a BNP Paribas mortgage?

BNP Paribas isn’t the easiest bank in Poland to borrow from. Here are the basics:

- Minimum 20% down payment is required

- Your income must be in PLN

- Non-EU citizens need a valid residence card (valid for at least 3 months after application?

- EU citizens need a certificate of registration of residence

The bank accepts most common types of income (employment contracts, casual contracts, self-employment, rental income), but doesn’t count things like dividends, umowa o dzieło, social benefits, or income from abroad. Buy-to-let mortgages also aren’t available.

How much can you borrow from BNP Paribas?

BNP Paribas is known to be one of the stricter banks in Poland. Borrowing limits are usually lower than at competitors. Examples (assuming no other loans, applicants aged 20–40, employed on contract):

Single person

Monthly net income → Max loan

5,000 PLN → 218,000 PLN

7,000 PLN → 311,000 PLN

10,000 PLN → 449,000 PLN

13,000 PLN → 588,000 PLN

Couple without children

Monthly net income (combined) → Max loan

8,000 PLN → 357,000 PLN

11,000 PLN → 495,000 PLN

15,000 PLN → 680,000 PLN

20,000 PLN → 911,000 PLN

Couple with children

Monthly net income (combined) → Max loan

8,000 PLN → 269,000 PLN

11,000 PLN → 495,000 PLN

15,000 PLN → 680,000 PLN

20,000 PLN → 911,000 PLN

Pros and Cons of BNP Paribas Mortgage

Pros:

- Competitive interest rate (from 5.9%)

- Fast approval process (1–2 weeks on average)

- No arrangement fee

- No early repayment penalty

Cons:

- High entry requirements (20% down payment, stricter income checks)

- Lower maximum borrowing capacity compared to other banks

- Limited choice: only 5- or 10-year fixed rates available (no variable rate mortgages)

Final Thoughts

Mortgage rates in Poland are finally easing, giving buyers more room to plan property purchases. BNP Paribas currently leads with the most attractive offer, but strict requirements and borrowing limits mean it won’t be the best option for everyone.

My advice: Always compare offers from multiple banks. Interest rates matter, but don’t forget about additional costs, insurance requirements, and maximum borrowing limits.